SMM, June 21:

This week, the Guangdong Exchange shifted its contract focus from the 2507 contract to the 2508 contract. Under the backwardation structure, spot premiums/discounts in Guangdong rose from 210 yuan/mt on June 16 to 400 yuan/mt on June 17, before subsequently declining. So, how will spot premiums/discounts in Guangdong evolve under the current fundamental conditions?

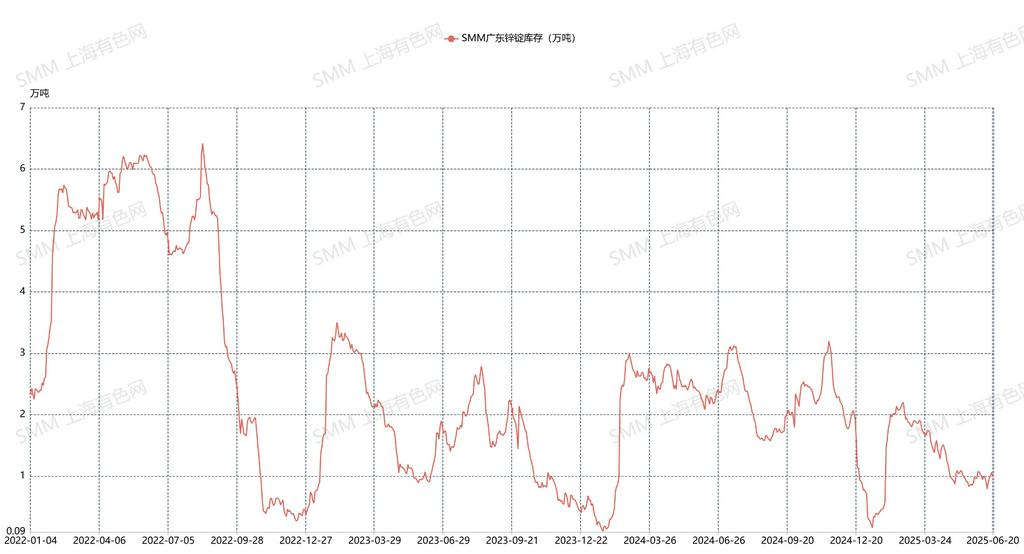

Supply side, with the normal production and gradual resumption of production at some smelters in South China, south-west China, and Central China in June, SMM expects zinc ingot production this month to reach 590,200 mt, a MoM increase of 40,800 mt. Smelters in South China and south-west China are expected to significantly supplement spot supply in Guangdong. Data shows that as of Friday (June 20) this week, social inventory in Guangdong stood at 10,100 mt, up 1,200 mt from Monday. Although current social inventory in Guangdong remains at a relatively low level, driven by the gradual production increases and the conclusion of maintenance at some smelters in south-west China, spot supply in the Guangdong market is expected to gradually rise.

Demand side, Guangdong is home to a large number of alloy enterprises, which have significant demand for zinc ingots. In terms of the monthly operating rate of die-casting zinc alloy enterprises, the operating rate of die-casting zinc alloy enterprises was recorded at 47.10% in May, a MoM decrease of 2.61%. The operating rate of die-casting zinc alloy enterprises is expected to continue to decline to 46.17% in June. As the market has entered the seasonal off-season for consumption, end-use demand will gradually weaken.

Now, let's examine the consumption situation in various sectors:

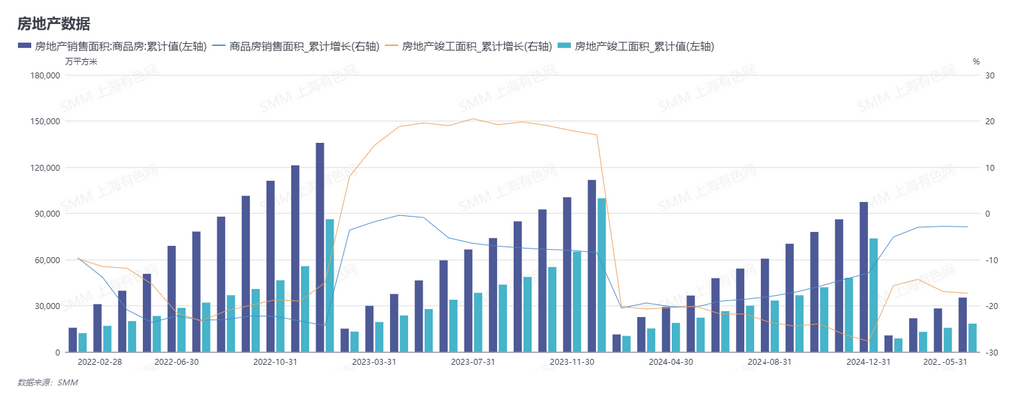

Real Estate Sector : The State Council executive meeting held on June 15 pointed out that a new model for real estate development will be established to promote the stable, healthy, and high-quality development of the real estate market. Meanwhile, as of May, the cumulative decline in China's commercial housing sales area was recorded at 2.9%, and the cumulative decline in the completed area of real estate projects was recorded at 17.3%. Judging from the performance of real estate data in the first half of 2025, the overall operation of China's real estate market is primarily focused on "stability," which does not offer significant bright spots for boosting downstream consumption of die-casting zinc alloy.

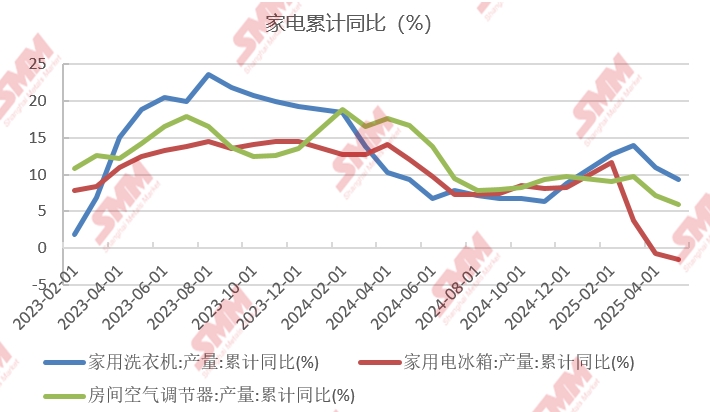

Home Appliance Sector : As of May, the cumulative production of household washing machines, household refrigerators, and room air conditioners in China increased by 9.3%, decreased by 1.5%, and increased by 5.9% YoY, respectively. Home appliance consumption, which performed well in the first half of last year, is in the doldrums this year. Despite the increase in the number of home appliance subsidy categories and the increase in subsidy amounts in China in 2025, the demand for home appliance replacements among domestic households has relatively weakened due to the partial release of replacement demand by last year's subsidy policies. Meanwhile, under the influence of tariff disruptions and local geopolitical factors in the first half of the year, certain resistance may be formed to China's home appliance exports.

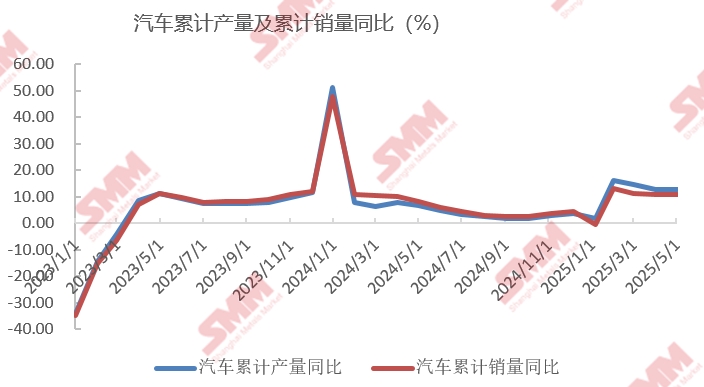

Automotive Sector: As of May, China's cumulative automotive production and sales recorded YoY increases of 12.7% and 10.9%, respectively, remaining basically flat compared to the previous month's data. However, as we approach the end of Q2, June to August is typically the off-season for automotive sales in China. It is anticipated that the demand for die-casting zinc alloy from the automotive sector will gradually weaken.

Additionally, in the luggage zipper and electronics sectors, these two sectors account for a relatively small share in the die-casting zinc alloy market. Except for some enterprises in South China that have relatively stable demand due to their downstream customers, the overall market performance is also weak. In terms of export orders, enterprises that previously performed well in export orders have also seen a decrease in order volumes recently. With only 52 days remaining until the 90-day suspension period for China-US tariffs expires today, and amidst the tense situation in the Middle East, there remains significant uncertainty in the subsequent development of export orders. Therefore, it is expected that the subsequent market demand in Guangdong will gradually decline under the influence of seasonal consumption off-season and export uncertainties.

In summary, given the increase in supply and the gradual weakening of demand, it is anticipated that premiums and discounts in the Guangdong market will continue to show a downward trend in the near future.

(The above information is based on market collection and comprehensive assessment by the SMM research team. The information provided herein is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make prudent decisions and should not rely on this information to replace their own independent judgment. Any decisions made by clients are unrelated to SMM.)